What happened to the Rishi Sunak I knew at school?

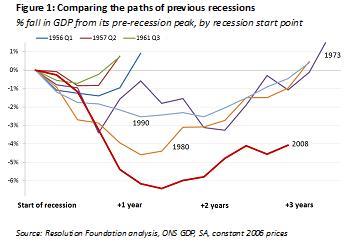

So, what will the chancellor hope to see next Tuesday? Exports and investments will be important, but improving household consumption should be at the top his list. The graph below compares what

has happened to household consumption over this recession with previous ones (it displays the double-dip recessions of 1973 and 1975 with a single line.) After each of the three earlier

downturns, consumption growth recovered much faster than it has this time. On each occasion, that powerful upward pull helped to lift the economy to recovery. Not so this time.

The reason for this might be that the UK is rebalancing away from domestic consumption towards exports, but there’s no ignoring the fact that consumption still makes up almost two thirds of

UK GDP. Sluggish household spending is a granite millstone around the neck of recovery.

The position of Britain’s households will therefore be critical to what we learn on Tuesday and that fact poses a conundrum. Consumer spending is anaemic mainly because of the squeeze on

disposable incomes. Real household disposable income has now been falling consistently since the start of 2009. In the first quarter of this year, it was £8bn below its peak in the final

quarter of 2008. That’s its deepest fall since comparable data began in 1955, and the likelihood of continued high inflation, low wage-growth and cuts suggests that it may have some distance

further to go.

This means that consumption is increasingly dependent on households eating into their savings. The household savings ratio is falling, and from a low base. Again, the graph below

compares recent recessions. In all cases, households entered previous downturns in a much better borrowing position than they did in 2008. And after a brief recovery in 2009, the

savings ratio is now falling again. The OBR itself suggests that the savings

ratio will fall further in coming months. But with McKinsey’s analysis (p.12) suggesting that the UK household sector will begin to deleverage in the near

future, it seems unlikely that expending savings will prove a sustainable route to recovery.

Needless to say, these are uncomfortable truths for a government whose entire economic narrative is based on reducing our reliance on debt, and whose fiscal strategy will hit household incomes hard

in the coming months. The hope, of course, is that next week will lay some of these fears to rest. If not, we face the prospect of either a slow recovery or one that’s increasingly

reliant on household debt.

James Plunkett is Secretary to Commission on Living Standards at the Resolution Foundation and is onTwitter.

Comments

Join the debate for just $5 for 3 months

Be part of the conversation with other Spectator readers by getting your first three months for $5.

UNLOCK ACCESS Just $5 for 3 monthsAlready a subscriber? Log in