It’s odd to read headlines today saying that the UK has officially entered recession. We’ve known this for months: shops were closed, restaurants shuttered. You couldn’t get a cup of coffee or a haircut, offices were closed and millions furloughed. These were not normal times – but we knew that then, as we know it now. What we didn’t know was how far the economy had contracted, and how much this could be remedied by ending lockdown. The big news today, revealed by official figures released by the Office for National Statistics this morning, starts to answer this.

It turns out that our economic hit was one of the hardest in Europe. UK GDP fell 20.4 per cent in the second quarter of the year (ie, April, May and June), its largest quarterly slump, and worst recession, on record. No part of the economy was spared but the services sector fared particularly badly, falling by 20 per cent, with the worst hit to accommodation and food services. To the surprise of no one, putting the nation under strict lockdown sent the economy into a free fall.

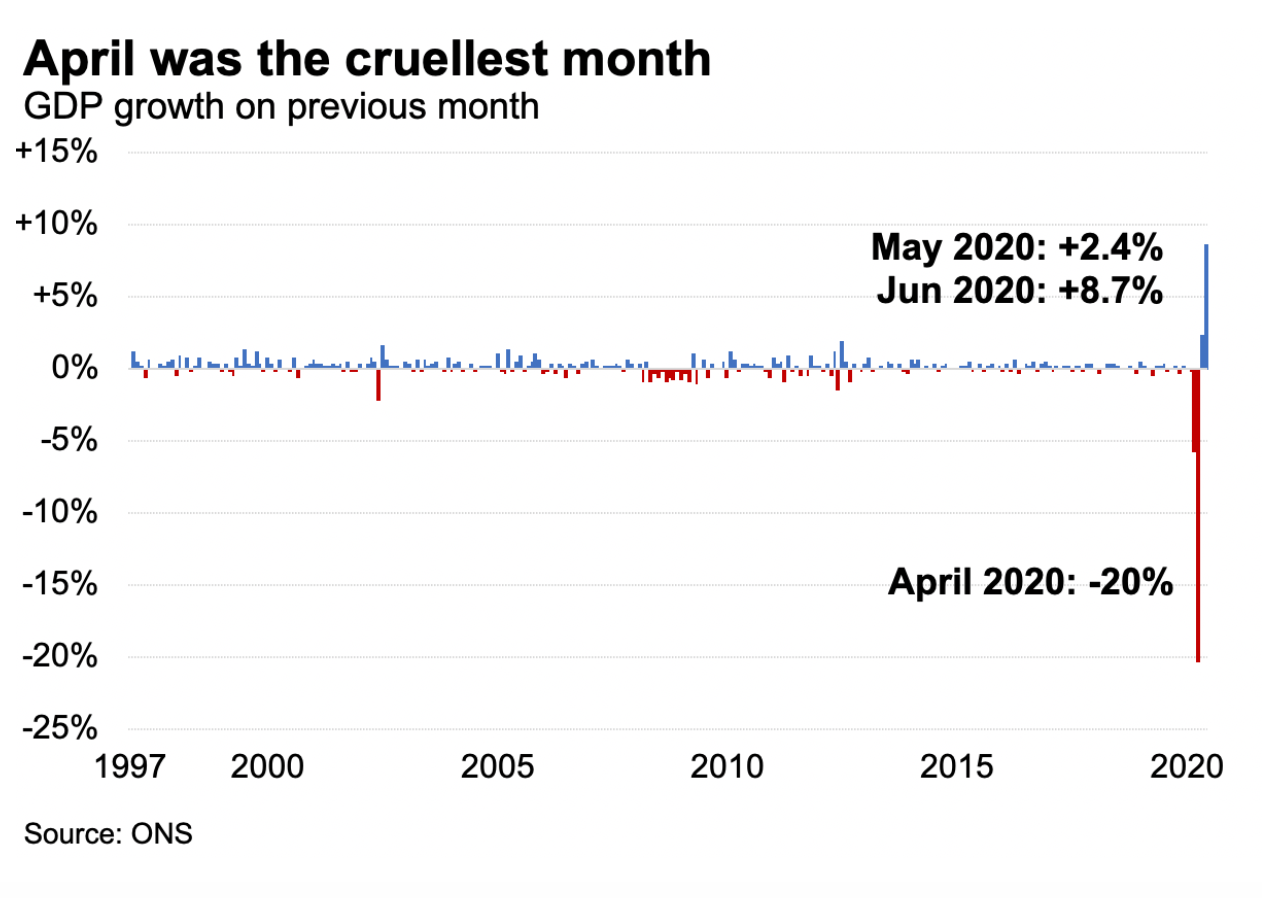

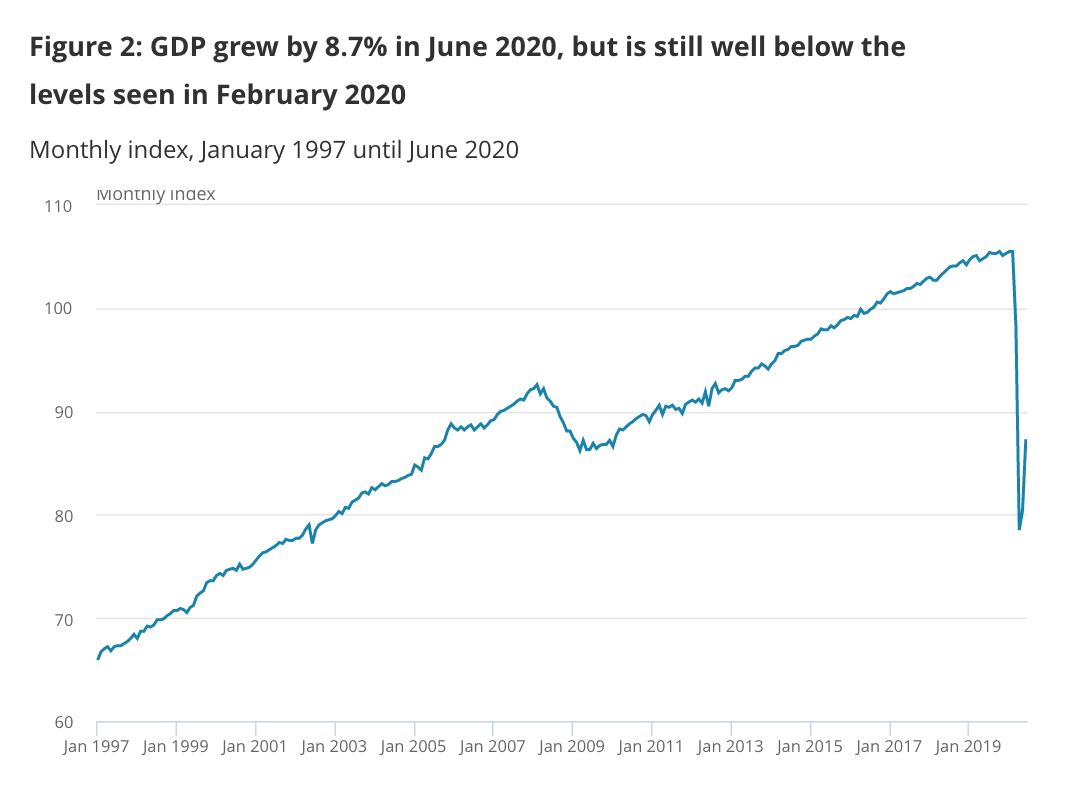

But while the whole of Q2 adds up to a 20.4 per cent contraction, the fall only came in the month of April. According to ONS figures, the economy has started its comeback: a revised 2.4 per cent growth in May (up from 1.8% on initial estimates) and nearly 9 per cent growth in June.

That growth levels in June were far more buoyant than May’s figures signals that reopening non-essential shops made a significant difference to economic activity, and the further reopening of pubs, restaurants, hairdressers and other retail outlets in July could result in an even bigger boom in next month’s figures. As of the end of June, the UK economy is around 17% smaller than pre-crisis levels – this is better than April, when it was 25% smaller. The irony of course is that as we get the official figures for the Covid recession, we are also heading out of it: all economists agree that Q3 (which we entered last month) will show a recovery – as you’d expect when you start allowing for economic activity which was temporarily banned by the government. But the pain caused by two quarterly contractions will still be felt acutely, for months, possibly years. And we’re still a long way off achieving a complete, V-shaped recovery, the likes of which will be determined by decisions made around the economy next .

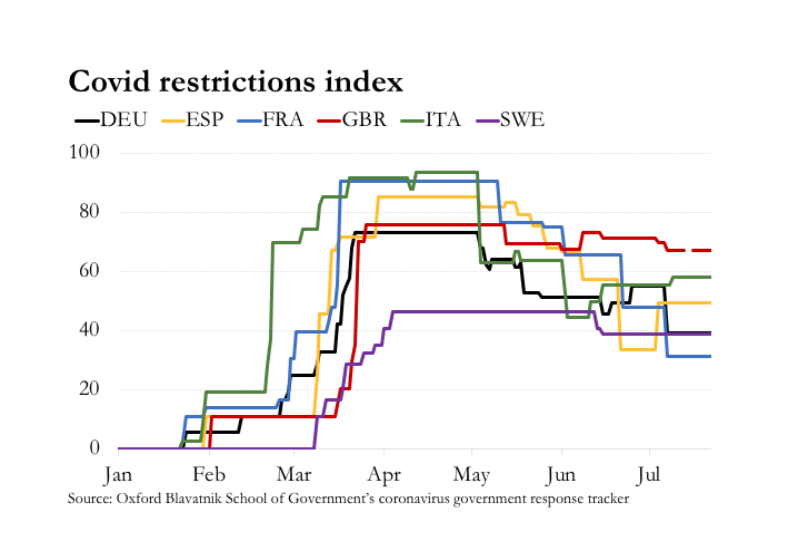

Those who are claiming today that Britain has experienced one of the worst contractions in Europe because it was late into lockdown are only right if we consider that the delay in March is a major reason why the government has been so cautious to re-open the economy, trailing European countries by weeks, sometimes months. As the ONS has previously pointed out, the link is between the economy and the stringency of lockdown: the harsher the rules and restrictions, the more damage that’s done to the economy. This partially explains the Q2 figures today, and bodes ill for the next few months: the Blavatnik School of Government at Oxford University keeps a regular update of stringency measures and finds Britain is, still, the worst in Europe.

While the index of services still shows almost all sub-sectors having yet to make a full recovery, it is not obvious there will be scope, or permission, to make a full recovery soon. Out of education, arts, entertainment, food, accommodation and recreation, some sectors have yet to reopen, or return to full capacity. They underline concerns that, over the course of the year, the UK economy will end up having taken the biggest Covid hit in Europe – with the largest increase in deficit of any major economy.

Of course we were going to fall. Now we know how hard. The outstanding question still is how fast will the recovery be.

Comments